Budgeting and the Federal Credit Reform Act of 1990: An Explainer

The Federal Credit Reform Act of 1990 (FCRA), enacted as part of the Budget Enforcement Act (P.L. 101-508), established separate budgetary treatment for credit programs, shifting from standard cash accounting to a new method that more accurately represents the cost of these programs over time. FCRA resolved a long-standing issue for Congress in comparing the costs of direct loan programs with guaranteed loan programs. By better reflecting the true economic subsidy provided by credit programs generally, FCRA helps Congress better allocate budgetary resources to serve the American people more effectively, efficiently, and sustainably.

FCRA has four stated purposes: to "(1) measure more accurately the costs of Federal credit programs; (2) place the cost of credit programs on a budgetary basis equivalent to other Federal spending; (3) encourage the delivery of benefits in the form most appropriate to the needs of beneficiaries; and (4) improve the allocation of resources among credit programs and between credit and other spending programs." FCRA budgetarily recognizes that loans have regular, contractually required cash flows that occur over the long life of a loan, not just in the year the loan gets made. This primer presents the history, purpose, and requirements of FCRA to answer the questions of why it was needed, how it developed, and what it does to help Congress make the best decisions to support Americans.

Credit programs are an important way for the federal government to offer financial assistance

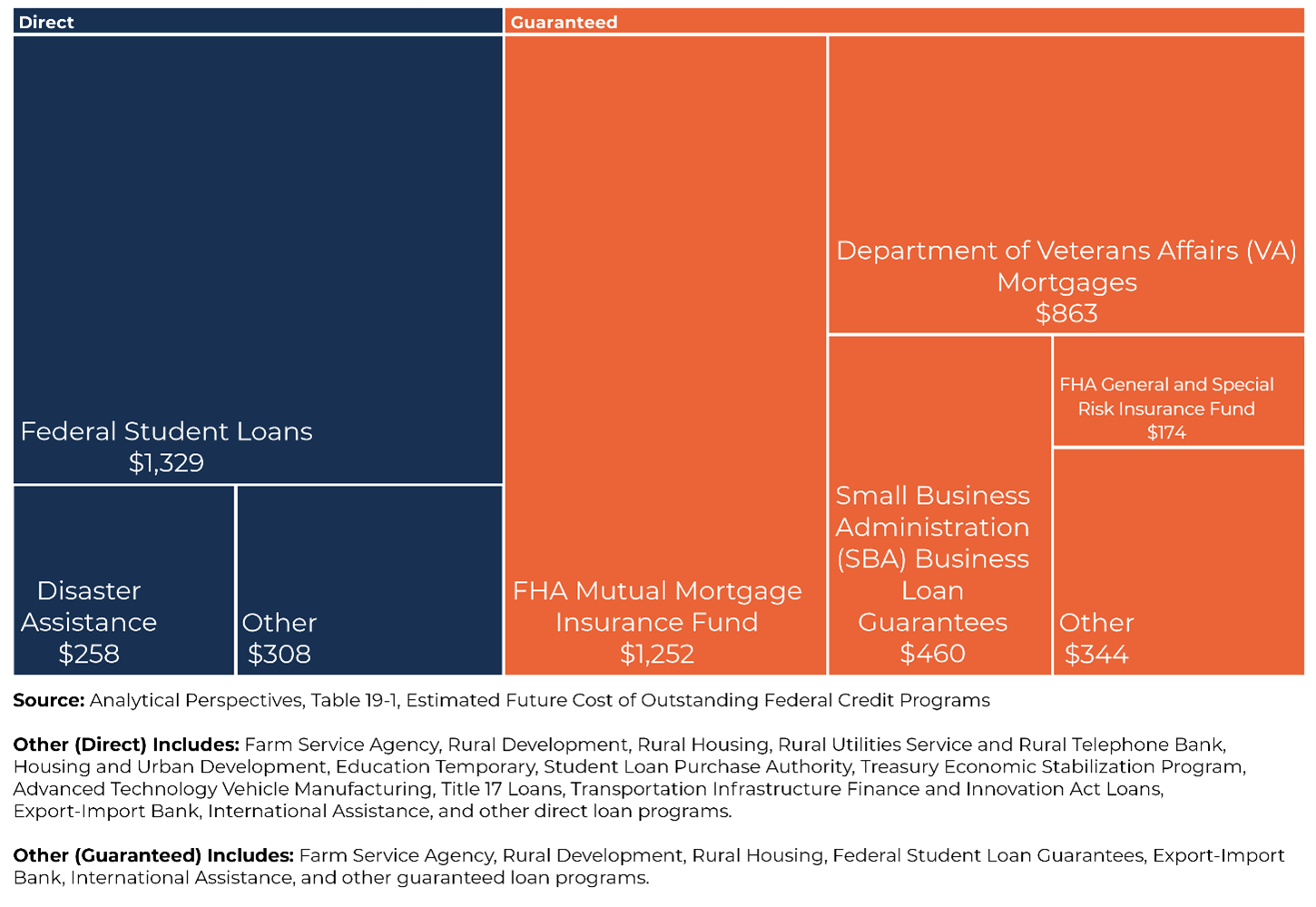

Since as early as the 1930s, the federal government has used credit programs to offer financial assistance to Americans. These credit programs involve making loans to individuals, businesses, or other entities (called direct loans) and guaranteeing payments on loans made by private lenders (called loan guarantees). One of the federal government's largest guaranteed loan programs today is also one of its oldest: Congress established the Federal Housing Administration (FHA) in 1934, to help Americans access mortgages at a time when the housing industry was in dire straits. Since then, loan programs have expanded to support communities across America, with nearly $5 trillion in outstanding credit across the federal government as of the end of 2021.[i]

More Information [i] | For more information on the federal government's credit portfolio, see Table 19-1, Office of Management and Budget, Analytical Perspectives Chapter 19, Credit and Insurance. |

Many government agencies have loan programs that directly lend to borrowers, including the Department of Education (direct loans to students), the Department of Agriculture (direct loans supporting farmers and rural development projects), and the Federal Emergency Management Agency (emergency lending to communities struck by natural disasters). Other government agencies offer loan guarantees to lenders to expand access to private credit, such as the Department of Housing and Urban Development (FHA's mortgage guarantees), the Small Business Administration (guarantees such as the Paycheck Protection Program), and the State Department (guaranteed lending to sovereign nations like Ukraine). The federal government also guarantees groups of already-guaranteed loans like the Government National Mortgage Association's mortgage-backed securities. These secondary guarantees facilitate important secondary markets for institutional investors.

Outstanding Federal Credit Portfolio, 2021 (In Billions of Dollars)

FCRA enables better comparisons of different types of assistance

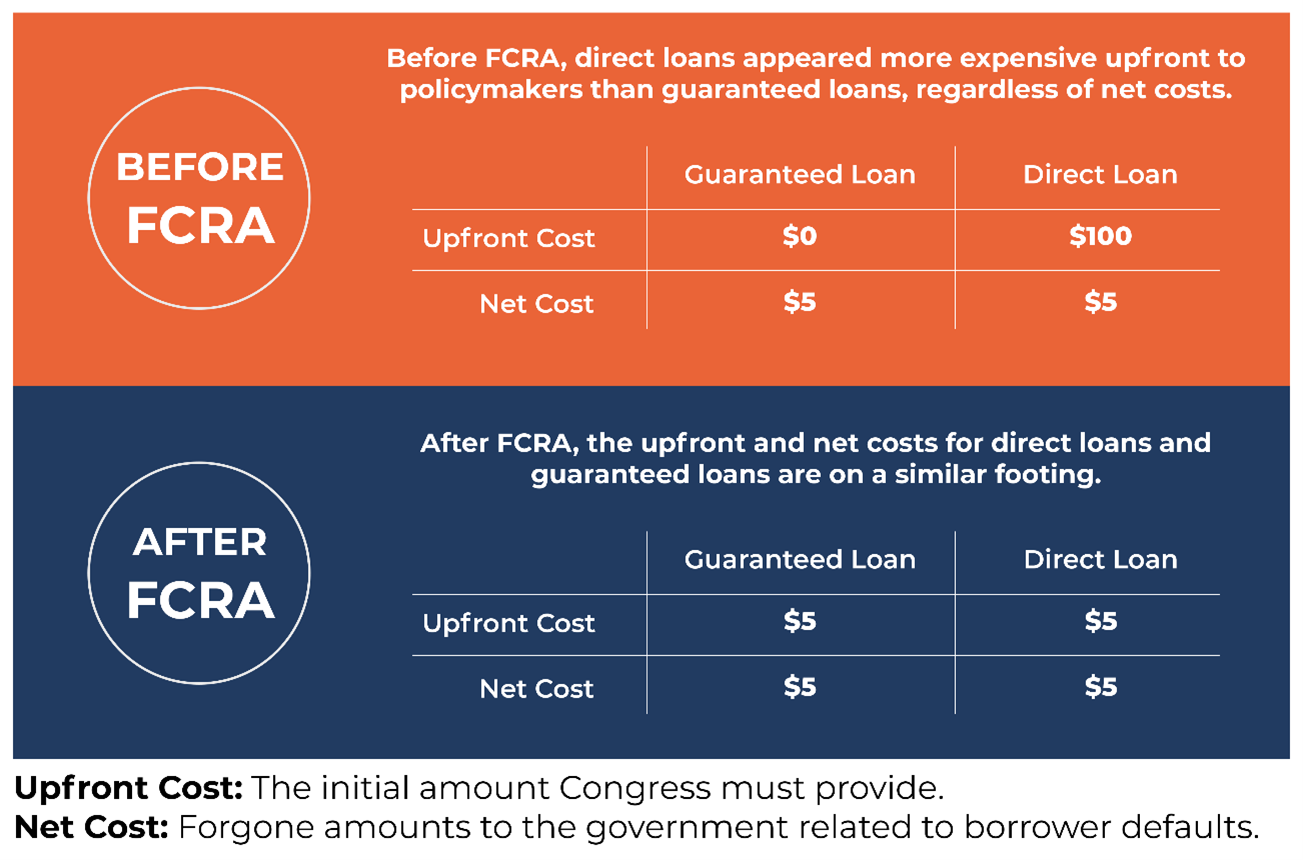

Before FCRA's implementation in 1992, direct loans and loan guarantees were budgeted and accounted for on a cash basis, just like grants and other traditional forms of government assistance. Under prior cash accounting methods, costs were recognized and reported when money left the Treasury to go to borrowers or lenders, and receipts were recognized and reported when money was repaid.[ii] This led to issues with comparing grants, direct loans, and guaranteed loans, since only the cash paid and received during a current fiscal year were recorded in the yearly budget.

More Information [ii] | For more information on cash accounting, see Congressional Budget Office, Cash and Accrual Measures in Federal Budgeting. |

Cash budgeting would often cause confusion when Congress was comparing the cost of a direct lending program with a guaranteed lending program. Before FCRA, the cost of direct loan programs and guaranteed loan programs could look very different based on when cash flows were expected to occur, even if the programs supported the same borrowers and intended to provide the same amount of financial support over time. Whereas direct loans often distribute cash early in the life of the loan and receive gradual repayments over time, guaranteed loans often receive up-front fees and pay out claims to lenders over time. Due to these timing differences, direct loan programs looked expensive, while guaranteed loan programs looked inexpensive or free at the time the loan was made. This gave Congress an incentive to use loan guarantees to support Americans over direct loans due solely to when the accounting process recognized costs, rather than a real debate on the best way to deliver benefits to Americans.

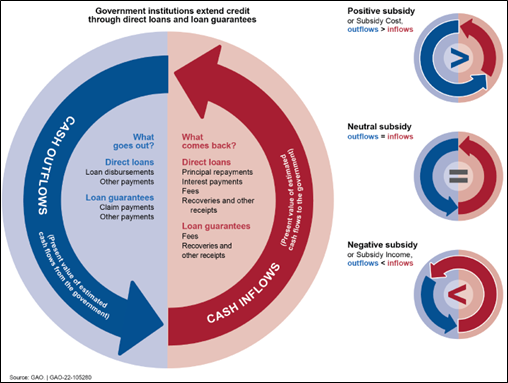

Credit programs often have much more complicated cash flows than traditional financial assistance, such as grants or tax breaks. Credit programs have cash flows that occur on a regular, often predictable schedule, set by contracts and legal agreements. These cash flows can include inflows like upfront fees, annual fees, interest payments, and principal payments. They can also include outflows like loan disbursement or claim payments to private lenders (for guaranteed loans). Cash flows can occur quarterly, annually, or on a different schedule, such as a balloon payment that occurs at the end of the life of the loan, depending on the contractual agreements with the borrower.

Example Of Upfront and Net Costs for Direct and Guaranteed Loans Before and After FCRA

Even before 1990, budgeteers had been thinking about the tricky problem of how to compare grants, direct loans, and loan guarantees when assessing government assistance. The President's Commission on Budget Concepts of 1967, which laid out many of the concepts still used in federal budgeting today, noted a need to better reflect the subsidy, or benefit offered to the borrower, over the whole life of the loan, to allow direct comparisons with other forms of assistance benefiting Americans. A grant of $100 has a different economic effect on a recipient than a loan of $100; this difference was not always clear under cash accounting. FCRA aimed to put the scored costs of direct loans, loan guarantees, grants, and other assistance on equal footing through the idea of a "subsidy rate", or the long-term cost to the government of a loan or loan guarantee that accounts for all the estimated inflows and outflows over time. This "subsidy rate" concept allows Congress to compare the actual federal costs of different types of programs more accurately.

FCRA pertains only to direct loans and loan guarantees made to non-federal borrowers

FCRA's budgetary treatment applies only to direct loans and loan guarantees to non-federal borrowers; it cannot apply to loans made to other federal agencies or for federal projects.[iii][iv]FCRA also exempts some specific insurance programs, such as the Federal Deposit Insurance Corporation, National Credit Union Administration, National Flood Insurance, and Crop Insurance, among others. While these insurance programs can share similar aspects with guaranteed loan programs, they are not loan guarantees.

FCRA specifically cannot apply to loans to federal borrowers or for projects that ultimately rely on federal funding. This ensures that FCRA does not violate conceptual issues raised by third-party financing.[v][vi] A loan where the expected source of repayment is future federal appropriations could look low-cost to the government today if budgeted under FCRA, but would understate the true cost to the federal government of these projects. If a borrower's ability to repay is entirely contingent on future Congressional funding decisions, the budgetary implications are fundamentally different from a loan where ability to repay depends on factors outside federal control. Scoring loans to federal borrowers or for federal projects using FCRA treatment would inaccurately skew preferences toward a project financed through borrowing, rather than a project directly funded by appropriations, even though the ultimate budgetary impact of both projects would be the same. The President's Commission on Budget Concepts of 1967 laid out the conceptual framework for determining if a project or end borrower should be included in the federal budget, including the project initiation and selection, the extent of governmental control, the economic ownership interest, and the source of repayment or income from the project's operation (such as future federal appropriations). [vii]

More Information [v] | For more information on third party financing, see Congressional Budget Office, Third-Party Financing of Federal Projects. |

More Information [vi] | For more information on federal and non-federal borrowers, see Government Accountability Office, Transparency Needed for Evaluation of Potential Federal Involvement in Projects Seeking Loans. |

More Information [vii] | In 2020, the Environmental Protection Agency, the Office of Management and Budget, and the Treasury Department published more detailed information about the criteria that would indicate if a project or borrower is federal for one of its large direct loan programs, the Water Infrastructure Finance and Innovation Act Program, in the Federal Register. |

FCRA's budgetary treatment applies only to financial support given to a non-federal borrower "under a contract that requires the repayment of such funds with or without interest" (emphasis added, 2 U.S.C. § 661a(1)). Other governmental activities, such as offering grants or purchasing equity investments, may generate potential future returns to the economy and/or the budget, but such potential returns are not contractually obligated. Moreover, estimating those amounts presents unique forecasting challenges. Budgetary estimates of alternative policies being considered by Congress generally exclude such speculative dynamic effects, although dynamic estimates are sometimes available as supplementary information to aid decision-making.

In limited and unique circumstances, Congress has enacted certain exceptions to FCRA, applying it to specific programs that may not meet the strict definition of a direct loan or loan guarantee. Most notably, Congress enacted the Troubled Asset Relief Program (TARP) [division A of the Emergency Economic Stabilization Act of 2008; P.L. 110-343], as an emergency response to the financial crisis of 2008. It combined traditional loan programs with other forms of assistance, such as purchases of preferred stock and other financial instruments.[viii] Congress applied FCRA's budgetary treatment to TARP, with unique caveats in the discount rate used to calculate the final subsidy rates for these programs, to best represent that this support shared similar aspects with credit programs (such as cash inflows from preferred shares purchases), though it was more vulnerable to market risks.

More Information [viii] | For more information on TARP programs, see Congressional Budget Office, Report on the Troubled Asset Relief Program—May 2022. |

FCRA defines the cost of loan programs as the long-term cost to the government, in today's dollars

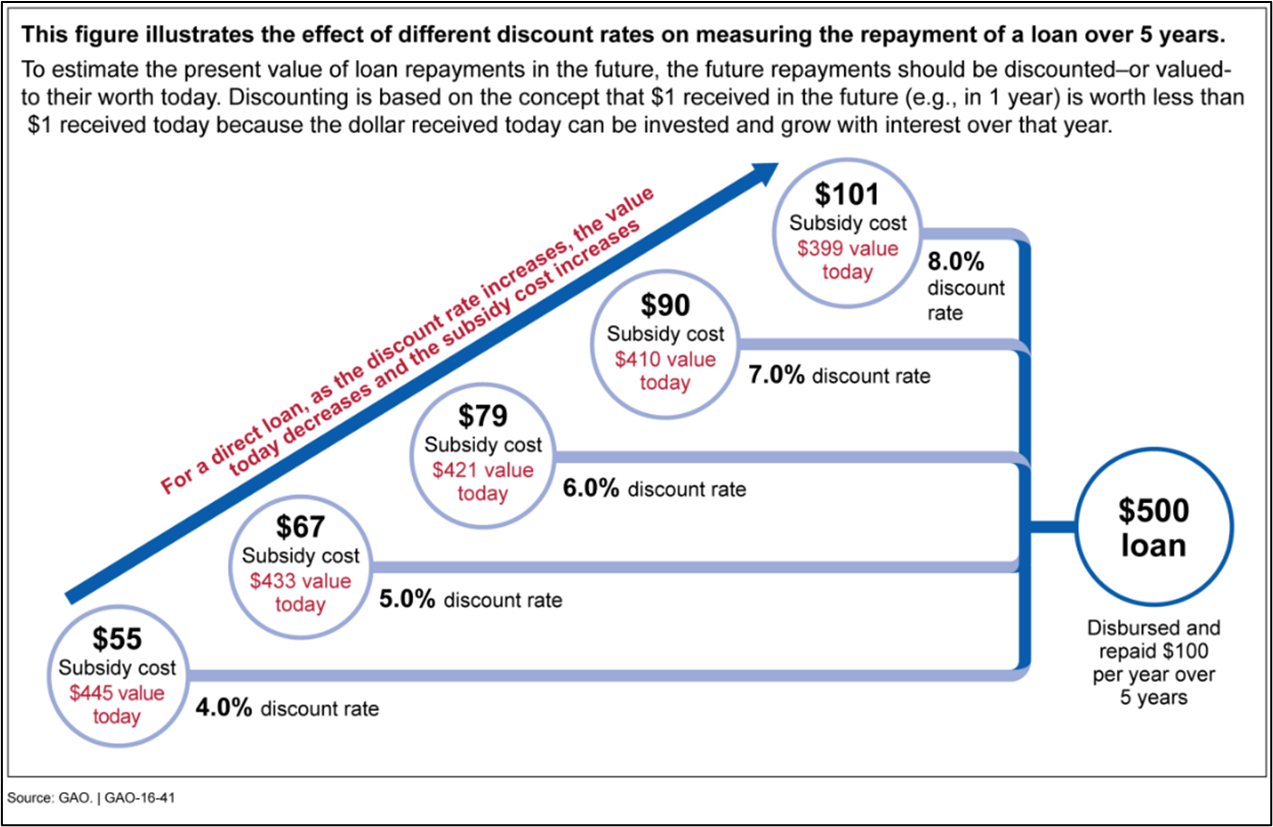

The key element of FCRA is its requirement that the budgetary cost of a federal lending program be recorded as the estimated long-term cost to the government over the life of the loan, in today's dollars, discounted using Treasury interest rates. This cost, divided by the total amount of money lent out, is referred to as the "subsidy rate," since it is the subsidy that the government offers the end borrower per dollar. [ix] A loan program with a subsidy rate of 50 percent, for example, means that for every dollar lent out, the government expects 50 cents to be repaid over time and 50 cents to be provided as a benefit to the borrower through appropriated funds, in today's dollars.

Agencies and the Office of Management and Budget together assess the subsidy rates of each credit program offered by the federal government. [x] Multiple factors contribute to the estimated long-term cost to the government of a loan program, including loan characteristics (such as the final interest rate or repayment structure) and borrower characteristics (such as credit score), plus broader economic projections (such as house price appreciation or employment rate forecasts). To assess the total cost of a loan program in today's dollars, FCRA discounts future cashflows back to today using the interest rate on marketable Treasury securities that mature at a similar time. FCRA refers to the subsidy rate as being "calculated on a net present value basis," meaning the subsidy rate represents all the money flowing into the government and flowing out of the government (the net), in today's dollars (the present).

More Information [ix] | For more information, see Government Accountability Office, Current Method to Estimate Credit Subsidy Costs Is More Appropriate for Budget Estimates Than a Fair Value Approach. |

More Information [x] | For more information, see Office of Management and Budget, FY2023 Federal Credit Supplement. Subsidy rates are published annually for all credit programs as part of the President's Budget in the Appendix. The Federal Credit Supplement provides more detailed information about the subsidy rates and is published each year as supplemental materials to the President's Budget. |

Effect of Discount Rates on the Value of Loan Repayments and Subsidy Costs for a Direct Loan

Depending on the different borrower and loan characteristics mentioned above, credit programs can have a positive subsidy rate (greater than zero) or a negative subsidy rate (less than zero). A positive subsidy rate indicates that the borrower is receiving some form of subsidization from the government, either in the form of interest rates that are below Treasury rates or through principal that is not expected to be repaid, or other assistance like interest supplements. A loan program with a positive subsidy rate presents a cost to the government. This cost is covered by appropriations; Congress provides funding to benefit Americans who use the program. A negative subsidy rate indicates that the government is expected to generate receipts, either in the form of interest rates that exceed Treasury rates, borrower or guarantee fees, or recoveries on a loan's collateral. While a loan program with a negative subsidy rate does not require appropriations, it does require authority and a loan limit set in statute to operate as part of FCRA's requirements. Negative subsidy rate programs perform important roles, even when they do not provide economic subsidies, through standardizing a market, expanding credit access, or establishing new lending options for borrowers.

Calculation of Subsidy Cost for Direct Loans and Loan Guarantees

FCRA set up a new account structure to track loans over time and provide regularly updated "reestimates" of costs

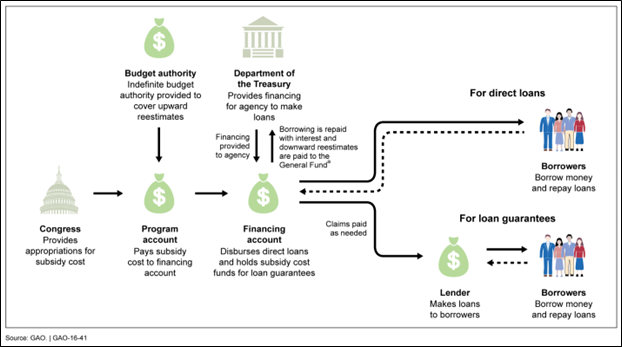

FCRA set up a new structure of accounts for loan programs to keep track of transactions over the life of the loan. This accounting structure is unique to credit and includes one account that records the appropriations that cover the subsidy cost of a lending program (the program account) and a second account that records the necessary transactions with the public and borrowers (the non-budgetary financing account).[xi] This dual account structure allows the budget to show both the subsidy that the government offers borrowers (or the receipts it collects) as the estimated long-term cost to the government in the program account, while also tracking the face value of the loans outstanding and other cash flows in the financing account.

More Information [xi] | For more information on the account structure for credit programs, see Office of Management and Budget, Analytical Perspectives Chapter 8, Budget Concepts and Budget Process. |

Federal Credit Accounts in Action

To help Congress and the public track the accuracy of these cost estimates, FCRA requires regular updates to the original subsidy rate of each loan program through annual "reestimates." Reestimates update the cost estimate for both new information from the past year (such as borrower performance or recovery actions) and revised forecasts (such as the latest projections of house price appreciation or unemployment). These reestimates are reported in the President's Budget. While reestimates do not impact the operations of a program, reestimated amounts are reflected in the debt and deficit, allowing the final cost of the loan to be accurately reflected in the deficit regardless of the original estimated cost.

FCRA resolved complex issues for federal credit programs

The federal budget provides vital information on the cost and scope of the government's activities and economic impact. Understanding the true cost and scope of government action is necessary for multiple stakeholders, including Congress as it uses its constitutional power of the purse to allocate resources; the Treasury as it manages cash and debt amounts; and most importantly the American people, as they evaluate how their government serves them. The Federal Credit Reform Act gives Congress a more accurate picture of the true budgetary cost and economic benefit of credit programs. These programs help Americans in a unique way, and therefore need unique treatment in the budget. While credit budgeting can be complex, solutions to America's toughest problems often are. The tools provided by FCRA for budgeting for credit programs allow Congress to best serve the American people.