Focus on Function: An Introduction

The annual Congressional budget process calls for Congress to lay out its fiscal policy goals for the next 10 years in the Congressional budget resolution. Through this process, Congress outlines how much revenue it wants to raise and how much money it wants to spend and for what purposes. The resolution is strictly a Congressional document and never goes to the President for approval.

As with any budget, the Congressional budget represents a statement of values. It lays out Congress' budgetary priorities and goals and the changes in revenues and spending necessary to achieve these goals. The resolution allocates spending across a set of functional areas, representing various national needs. The budget resolution and its accompanying report often provide only limited information about the changes assumed.

This "focus on function" report provides a detailed look at federal spending by function. It can be used to review any proposed budget resolution and understand the major programs that would be affected by funding levels included for that function. The following sections of this introduction provide background on concepts used throughout the function discussions.

WHAT ARE FUNCTIONS?

A function comprises a set of programs that serve a shared purpose or activity such as agriculture, health, or national defense. While some programs serve more than one purpose, they are generally assigned to a function based on their primary purpose. Occasionally, spending within a large program may be split between two functions.

The Office of Management and Budget (OMB) maintains the functional classification for federal accounts. It assigns new accounts and consults with the Congressional Budget Office and the Budget committees to evaluate proposed changes.

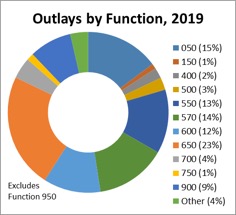

Each function is assigned a number, and the budget resolution lists spending by function in order by function number. Under OMB definitions, there are currently twenty functions. Six of these functions (functions 500 to 700), representing roughly 70 percent of federal spending, are primarily devoted to human resources. The national defense function accounts for another 15 percent of spending. Other functions make up smaller shares of overall spending.

Functions change over time; they have split apart and merged. At times, new functions are created just for the budget resolution. For example, for a number of years, the budget resolution has had a separate function for overseas contingency operations, whereas the President's budget allocates this funding to either national defense or international affairs, as appropriate.

| Function Name | Number |

| National Defense .............................................................................. | 050 |

| International Affairs ........................................................................... | 150 |

| General Science, Space, and Technology ....................................... | 250 |

| Energy .............................................................................................. | 270 |

| Natural Resources and Environment .............................................. | 300 |

| Agriculture ........................................................................................ | 350 |

| Commerce and Housing Credit ....................................................... | 370 |

| Transportation .................................................................................. | 400 |

| Community and Regional Development .......................................... | 450 |

| Education, Training, Employment, and Social Services .................. | 500 |

| Health ............................................................................................... | 550 |

| Medicare ........................................................................................... | 570 |

| Income Security ............................................................................... | 600 |

| Social Security ................................................................................. | 650 |

| Veterans Benefits and Services ....................................................... | 700 |

| Administration of Justice .................................................................. | 750 |

| General Government ........................................................................ | 800 |

| Net Interest ....................................................................................... | 900 |

| Allowances ....................................................................................... | 920 |

| Undistributed Offsetting Receipts .................................................... | 950 |

WHAT ARE BUDGET CATEGORIES, AND HOW DO THEY RELATE TO FUNCTIONS?

For more than two decades, most federal budget discussions and attempts to enforce fiscal discipline have revolved around the budget categories of discretionary and mandatory programs rather than function. Almost every function has both mandatory and discretionary programs.

Discretionary Programs ― Discretionary program spending is controlled through the annual appropriations process. In general, Congress provides a specific level of funding, and agencies can spend up to that amount. When evaluating the effect of budget policies on specific discretionary programs, analysts generally look at budgetary resources provided for the budget year and compare that to the prior year, the prior year adjusted for inflation, or another proposal such as the President's request.[1] Traditionally, the budget resolution serves to set an annual topline for discretionary spending, guiding the work of the Appropriations committees, although that role has been somewhat supplanted in recent years by statutory caps on discretionary funding.

Mandatory programs ― Mandatory program spending is controlled through authorizing legislation that establishes who – persons, households, or other levels of government – is eligible for what benefit, and/or who must pay what fees. When evaluating the impact of proposals on mandatory programs, analysts generally look at how much projected spending, or outlays, will change relative to continuing current law over a five- or ten-year horizon.[2]

The budget resolution itself does not show spending broken out by budget category. However, the accompanying committee report shows each of these categories broken out by function. (Note that the committee report shows both on and off-budget spending. The budget resolution itself includes only on-budget amounts. Social Security and Postal Service are the only off-budget programs.)

The detailed sections in this report discuss discretionary and mandatory programs separately.

HOW DO TAX EXPENDITURES FIT IN THIS ANALYSIS?

The federal government has a variety of tools to work toward meeting various national needs. It can directly provide assistance through federal spending programs. It can also use the tax code to create incentives for certain activity. Such subsidies play a role conceptually similar to government spending and are referred to as tax expenditures. These expenditures are revenue losses associated with provisions of the tax code that allow special exclusions, exemptions, or deductions or that provide special credits or tax treatments. In total, tax expenditures are larger than any given spending program. The detailed sections in this report discuss tax expenditures associated with each function.

The budget resolution process does not provide a mechanism for reviewing tax expenditures. Although the level of tax expenditures is an implicit component of the resolution's assumed revenue totals, the resolution itself provides no specific information on tax expenditures. The committee report accompanying the resolution does provide estimates of tax expenditures by function. However, the estimates are based on current law, not proposed policies.

OTHER COMMON WAYS OF CATEGORIZING FEDERAL SPENDING

The budget resolution is one of the only places where function is the primary level of decision making on federal spending. While the President's budget provides information in a variety of ways, its most detailed analysis is provided by agency. Enforcement of the budget resolution relies on an allocation of spending by committee, usually referred to as the 302(a) allocation after the section of the Congressional Budget Act that requires it. In this allocation, discretionary spending is generally allocated to the Appropriations Committee. Mandatory spending that requires action by the Appropriations Committee (known as an "appropriated entitlement") is also allocated to that Committee even though the level of spending for these programs is generally determined by authorizing statute. Most mandatory spending is allocated across authorizing committees.

The detailed sections in this report show how spending in a given function is allocated across agencies and committees. The distribution by committee shows appropriated entitlements with the authorizing committee that establishes program rules. Some funds that are unallocated in the budget resolution, primarily premiums, fees, and other offsetting receipts, are also shown with the authorizing committee that controls them.

The Appendix to this report displays the information in the reverse form: agency and committee allocations by function. The mandatory committee allocation in the appendix table shows appropriated entitlements and amounts unallocated in the 302 process separately within each authorizing committee.

Appendix Tables

Appendix Table 1: Discretionary Budget Authority by Agency and Function

Appendix Table 2: Mandatory Outlays by Agency and Function

Appendix Table 3: Discretionary Budget Authority by Appropriations Subcommittee and Function

Appendix Table 4: Mandatory and Net Interest Outlays by Committee and Function

[1] For most discretionary programs, budget authority (BA) – the legal authority to incur financial obligations – is the meaningful measure of budgetary resources. In the case of programs funded by certain transportation trust funds, the meaningful measure is obligation limitations. The program estimates provided in this document reflect CBO's spring 2018 baseline, which assumes spending remains at 2018 enacted levels adjusted for inflation, with one major exception. Funding designated as emergency spending, which is primarily for natural disaster response, is assumed to be one-time only.

[2] The estimates provided in this document reflect CBO's spring 2018 current law baseline, adjusted to exclude emergency funding beyond what has already been enacted.