From Lagging to Record-Breaking: How Democratic Policies Changed the Trajectory of Our Recovery and Secured Our Economic Outlook

Three years ago, in March 2020, the United States experienced the single largest job loss in any month on record, losing 1.4 million jobs in one fell swoop. The next month, that record was blown out of the water with a staggering 20.5 million jobs lost. By the Spring of 2020, COVID-19 was tearing through communities around the globe, and economic activity came to a sudden and near-complete halt as people sheltered to stay safe from a once-in-a-generation pandemic. Businesses were shuttering, and layoffs were broad, eminent, and swift. Over the coming months it became clear that the recession would be severe.

Indeed, in the first and second quarters of 2020, GDP growth fell by 4.6 percent and then a shocking 29.9 percent. Unemployment Insurance (UI) claims hit record highs with over 6 million claims in just a single week in April. Millions of Americans were out of work through no fault of their own and needed support to survive. Families were unable to put food on the table or keep a roof over their heads and all worried for the health and safety of their loved ones.

Looking back to where we were just three years ago, the progress we have made is extraordinary. Since February 2021, 12.4 million jobs have been created, and unemployment is near record lows of 3.6 percent. UI claims have returned to their historical levels, and GDP growth remains even. This historic recovery has had its fair share of inevitable challenges, including global inflation spikes fueled by ongoing universal supply chain issues and Russia's invasion of Ukraine. And while inflation peaked in the Fall of 2022 as the economy "reopened," it continues to fall and is expected to return to normal levels soon.

The available data underscore the strength and stability of our record-breaking recovery. Policy from President Biden and Congressional Democrats helped spur the fastest and most equitable recovery in decades. But this recovery was in no way guaranteed. The U.S. has greatly outpaced the rest of the world and our peer nations in terms of the speed and size of our recovery. Our nation's GDP growth has been swifter than Germany, France, Italy, and the UK. And inflation has increased in all these countries, but has fallen the fastest in the United States.

Not only has this recovery been faster than other nations, it also has been much faster than previous recoveries in the U.S. After the Great Recession in 2008, it took more than six years to recover all the jobs lost. In this recovery, despite losing 2.5 times more jobs in the worst of the crisis, we returned to pre-crisis jobs levels in just over two years – recovering more jobs in about a third of the time. Even when you compare the COVID crisis to the much milder recession in 2000, our economy still recovered nearly two years faster after the COVID recession.

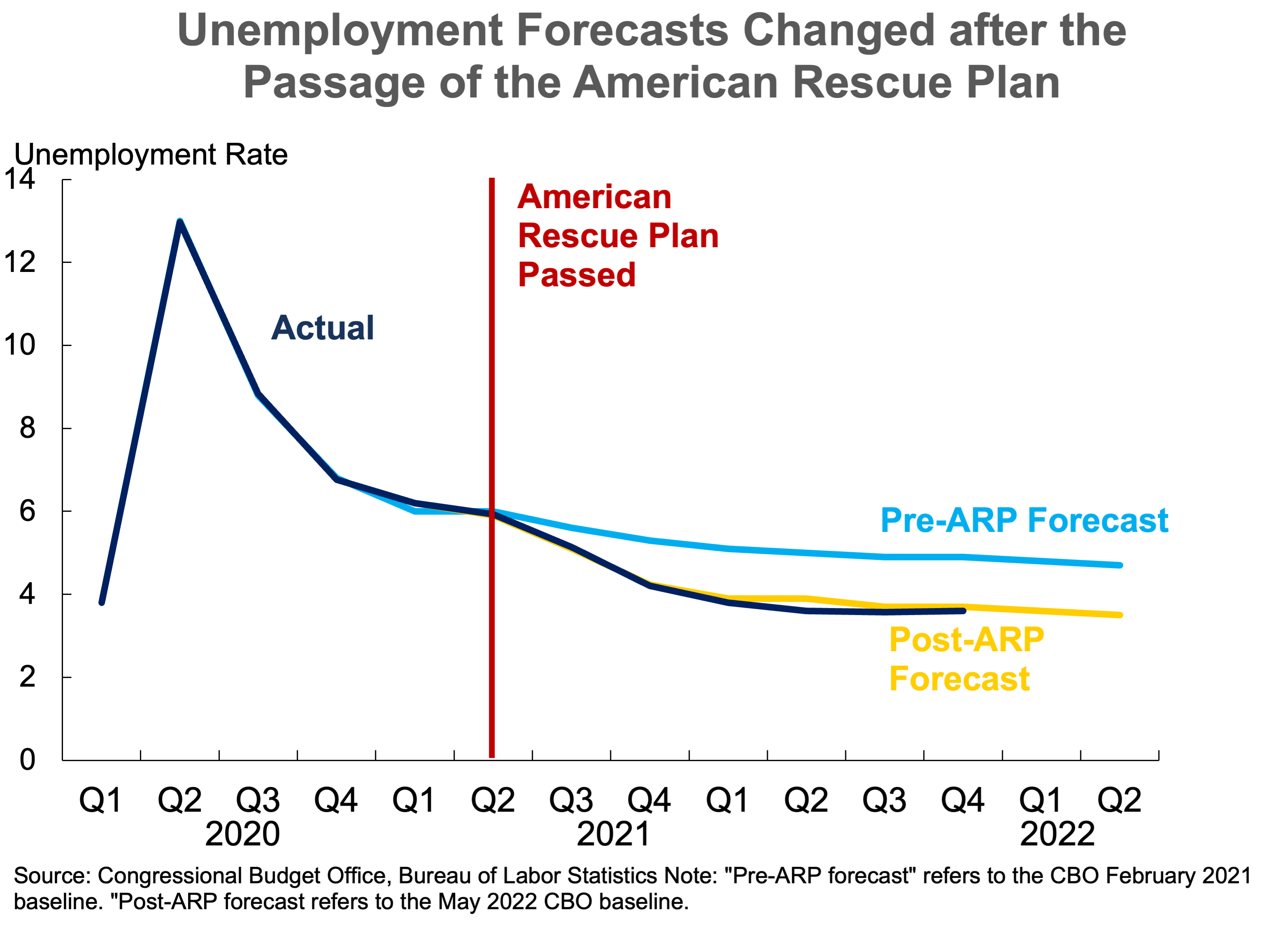

Such a swift and inclusive recovery was by no means guaranteed. So what made the difference? Strong fiscal support, primarily the American Rescue Plan (ARP), played a huge role. The ARP was passed in March 2021, at a time when the recovery still looked uneven and out of reach. Vaccine roll-out was just barely beginning, and COVID had surged brutally over the winter, taking nearly 200,000 American lives. Job growth was shaky and we remained more than 8 million jobs below pre-COVID levels. Most economists expected that the recovery would be prolonged and painful. We now know that – aside from delivering shots in arms and lifesaving relief – the ARP marked a turning point in our recovery, supported the creation of 4 million jobs, and helped to double GDP growth.

Even the nonpartisan Congressional Budget Office (CBO) dramatically changed its pre- and post-ARP projections. Prior to passage of the law, CBO assumed the economy would not reach full employment for at least a decade, but thanks in part to the ARP, we passed that benchmark in the Spring of 2022 instead. Not only that, unemployment fell for all groups, signaling we had achieved an equitable, "V-shaped" recovery, rather than a "K-shaped" recovery where the wealthy recover and working Americans are left behind.

Democrats have also used the last two years to build on this progress and ensure long-term economic growth and prosperity. The Infrastructure Investment and Jobs Act makes transformative investments in our nation's infrastructure by rebuilding roads, bridges and rails, improving access to clean water and high-speed internet, while tackling the climate crisis and creating millions of good-paying jobs. The CHIPS and Science Act will improve domestic manufacturing and supply chains while also creating good-paying manufacturing jobs. And the Inflation Reduction Act expands health care access while making investments in energy security and climate resilience, all while lowering energy, prescription drug, and other everyday costs for families. Taken together these policies will help create a more productive and resilient economy of the future.

With much credit due to Democrats' legislative achievements during the 117th Congress, our economy is back on track and Americans are poised to not only survive but thrive in this economy. However, without additional action and policies that continue to prioritize the advancement and well-being of working Americans and families, this progress is vulnerable. So far, our recovery has been able to withstand and even overcome unexpected global economic headwinds. But perhaps the greatest threat is the potential for self-sabotage. By refusing to raise the debt ceiling unless their demands for extreme and unworkable spending cuts are met, Republicans are choosing to impose an unnecessary crisis on the nation and prioritizing the super wealthy and special interests over the health, safety, economic security, and overall well-being of working-class Americans. This is dangerous and counterproductive to our long-term economic outlook. Financial markets, small to large businesses, and American workers need certainty and confidence that this recovery is not short-lived but a new trajectory for our nation's future.

President Biden's FY24 Budget provides Congress with a blueprint to accomplish this and more. By prioritizing responsible investments in America, lowering costs for families, protecting and strengthening Medicare and Social Security, and achieving $3 trillion in responsible deficit reduction, Democrats will build on the accomplishments of our landmark legislation, grow our economy from the bottom up and middle out, and strengthen our fiscal outlook for generations to come